In brief

- Because of the way it's built, Bitcoin suffers from slow transaction speeds and high transaction costs.

- The Lightning Network is a "second-layer solution" that speeds up transactions, while reducing costs, by skirting the main Bitcoin blockchain.

Bitcoin has been hampered by its own popularity. Thanks to the way the blockchain is designed, the speed of transactions is slow and the cost of transactions has increased.

Researchers, developers, and the Bitcoin community have been trying to come up with a way of allowing Bitcoin—and other cryptocurrencies—to accommodate more transactions.

Their best efforts to date have focused around something called the Lightning Network. Can it fix the cryptocurrency's scaling problems?

Speed and cost

A blockchain has two limitations we need to explain before exploring potential fixes.

The first is speed.

In a blockchain, blocks are essentially groups of transactions collected together. As part of a blockchain’s design, there are only so many transactions that can be included in a block.

If your transaction doesn’t make it into the current block, it joins a queue. That queue can take anywhere from a few minutes to potentially a day or more to process, depending on how many other transactions are queued in the mempool.

That limits the blockchain’s use as a medium to process quick transactions, like buying a cup of coffee. No one wants to wait around for the network to verify you’ve got the cash.

The second limitation is cost.

Bitcoin’s network, and others, are built upon a consensus protocol called proof-of-work.

This is where miners expend energy trying to solve a difficult puzzle. To help offset the cost of equipment and energy used in that calculation, miners charge transaction fees.

When the system is small, and the number of transactions that need verifying is few and far between, the network works well and transaction costs are low. As the network grows, however, so do transaction fees, since there is limited space in each newly mined block. As a result, transactions with the highest fees are prioritized for processing when the system faces high usage.

Bitcoin's scalability challenge became apparent toward the end of 2017 when millions of people jumped on the Bitcoin bandwagon and it struggled to cope with the number of transactions. At its peak in December 2017, the average cost to process one transaction on the Bitcoin blockchain—whether the amount was $1 or $1,000—was $37. That made Bitcoin largely uneconomical as a currency. And that’s where the Lightning Network comes in. (We've got a whole article explaining more about Bitcoin's limitations.)

What is the Lightning Network?

The Lightning Network is a layer-2 built on top of the Bitcoin network, meaning that it's built separately from the Bitcoin network but interacts with it. It’s made up of a system of channels that allows people or companies to move money between one another without needing to use the blockchain to verify the transaction.

It bears similarities to the current settlement system used by companies like Visa and Mastercard. When you pay for something, it’s not instantly settled. Instead, there’s a quick verification of funds from the buyer and the request from the seller—giving the green light for a transaction to take place. The actual settlement of funds happens later—in some cases, days or weeks.

The Lightning Network is run by a network of nodes that process payments, and transactions are commonly made using QR codes—instead of complex public keys. In theory, it could allow thousands, or even hundreds of thousands, of transactions to take place instantly, making small transactions economical.

The bottom line is, payments are faster and cheaper.

Who came up with the idea?

The Lightning Network has its origins in musings by Satoshi Nakamoto, the pseudonymous creator of Bitcoin, but was formalized by researchers Joseph Poon and Thaddeus Dryja, who published a white paper about the Lightning Network on January 14, 2016.

They argued that a network of micropayment channels could fix the scalability issues of the Bitcoin network, rather than changing the Bitcoin network itself to allow more transactions.

Lightning Labs, a blockchain engineering lab, helped to launch a beta version of the Lightning Network in March 2018—alongside a host of individuals and other companies including ACINQ and Blockstream. It was initially funded via a $2.5 million seed round, which included notable investor Jack Dorsey (whose company Square has since funded several grants for Bitcoin and Lightning Network projects). The first version of the Lightning Network was launched on Bitcoin in March 2018.

The Lightning Network was the first attempt at a second-layer solution, but others followed.

This is excellent @tippin_me ⚡️ https://t.co/FifrgwBOTp

— jack (@jack) February 20, 2019

How does it work?

The Lightning Network is faster and cheaper because it skirts the main Bitcoin blockchain.

It has an unstructured network set up around it. Channels are the ad hoc, peer-to-peer connections through which payments are made. Any number of payments can be sent in a channel.

The network is maintained by nodes that route payments. Nodes are run by everyday people—or corporations—running a program on their desktops, laptops, or Raspberry Pis. This keeps the Lightning Network decentralized.

To start using the Lightning Network, any amount of Bitcoin needs to be locked up in a payments channel. Then, it can be spent across the Lightning Network until the channel is closed.

When someone wants to receive a transaction, they create an invoice, a long alphanumeric string of digits—often represented using QR codes. The person who wants to make the payment simply needs to scan this invoice with their Lightning Wallet and confirm (by providing a digital signature) the payment.

When a payment is made, the confirmation is sent across the network to the person who originally made the request. This is known as a peer-to-peer network and means the processing of payments is not reliant on any one party. This typically happens in just a few seconds—hence the name "Lightning."

Since payments aren't made on the Bitcoin blockchain, they're not subject to long wait times and high fees. This means that much smaller payments, or micropayments, can be made for as little as one satoshi (one hundred millionth of a Bitcoin).

Once someone has finished using the network, they can close that channel and exit, and then use their BTC again on the standard Bitcoin network.

How do I use it?

Let’s say you want to transact with your local coffee shop. First, you’d need to send some Bitcoin to a wallet that requires more than one signature or key to release the funds.

These are commonly referred to as multisig wallets. In the case of the Lightning Network, it allows people to enter into an agreement that ensures a payment is received, effectively creating a balance sheet.

Every time you buy a cup of coffee a new balance sheet is created, and you sign it with your public key to reflect what’s left in your wallet as well as what’s in the coffee shop’s wallet.

If you don’t want to buy coffee anymore from that coffee shop, you can close the channel, and the resulting balance sheet is committed to the blockchain as a permanent record.

Payment disputes also can be settled by referring to the last signed balance sheet between the two parties.

What happens if you don’t have a direct channel with the next place you want to buy something from? The network will find the shortest route between you and the shop via others in the network.

How to connect

You can connect to the Lightning Network either by running a node or by using a Lightning wallet. Here are our top picks:

Bitcoin Lightning Wallet on Android

If you don’t want the full-node experience, you can download the Bitcoin Lightning Wallet app on your Android phone, which sorts everything out in the background. With this, you can open a Lightning channel and start making transactions with other users. It’s also “non-custodial,” meaning you look after your own keys—keeping your Bitcoin in your hands. (We tried it out by paying for a taxi ride).

Read our review of the Bitcoin Lightning Wallet.

Blue Wallet on iOS and Android

If you want to use the Lightning Network but don’t want to look after your own funds, Blue Wallet is a custodial service that runs a node for you. It allows you to send and receive Lightning payments, but doesn’t let you withdraw your Bitcoin from the Lightning Network.

Bitcoin full node

To get the full Lightning Network experience, you can try running a full node.

So what does this mean? Well, for a start, you’re now supporting the Bitcoin network and the Lightning Network by checking that transactions are legitimate. It also means you can connect it to your computer and make transactions from your own node. This literally makes you your own bank; you are the only person owning and controlling your funds. Scary, huh?

Eclair Lightning Node

If you’re feeling more ambitious, you could set up a full Lightning Node. This takes a lot more computer know-how. It means downloading Eclair onto your computer—or a homemade Raspberry Pi—and running it. You are then routing transactions on the network and can make your own transactions.

Eclair also offers a mobile version for Android users called Eclair Mobile. This is a stripped-down Lightning node, which means you stay in control of your Bitcoin. You can connect it to your own Eclair Lightning Node if you’re running one. There’s only one catch: You can’t receive payments. Eclair explains why in this blog post. (TL;DR: It’s safer and easier for them.)

Lightning Joule

Once you’ve set up your own node, what next? Are you stuck with using a desktop app? Lightning Joule is a browser extension that lets you connect your Lightning Node to your browser so that you can easily make payments within Chrome, Firefox, Opera, and Brave. It’s a convenient hack.

What can you do?

For a start, you can make payments to anyone else who has a Lightning wallet set up. But there’s more to the Lightning Network: As a digital currency, it's easily integrated into websites without the need for third parties.

Although the vast majority of crypto companies don’t yet accept Lightning transactions, that figure is slowly growing. Nonetheless, a wide range of popular Lightning-capable platforms are currently operating, ranging from cryptocurrency exchanges like Bitfinex and MercuriEX to online retailers and merchants like Bitrefill, plus a wide range of casinos and other service providers.

If you are looking for somewhere local, then you might be able to find something nearby on Accept Lightning or on the Lightning Network Stores.

Here are some examples of things you can do with the Lightning Network:

Get some satoshis with a Lightning Faucet

You can get some more Bitcoin. Faucets have long been a way to distribute small amounts of Bitcoin and other cryptocurrencies, and it’s no different with the Lightning Network. This Lightning Faucet lets you test sending and receiving from a Lightning wallet; you can withdraw 14 satoshis at a time, which is just over $0.004.

Tip people in Satoshis on Twitter

Do you wish social media was more rewarding? Well now it is. You can tip other people—and they can tip you—in Bitcoin using the Lightning Network. Simply integrate Tippin.me, and it puts a little lightning symbol on every tweet.

🤭 The Chrome extension that places a https://t.co/NVpjMUDdfJ button in every Tweet is here.https://t.co/Ra3de5dr50#LightningNetwork #LNTrustChain pic.twitter.com/FIx5zBbZfb

— Tippin (@tippin_me) February 14, 2019

You will need your own wallet to send tips (see above). All the cool kids are doing it, including Twitter co-founder Jack Dorsey.

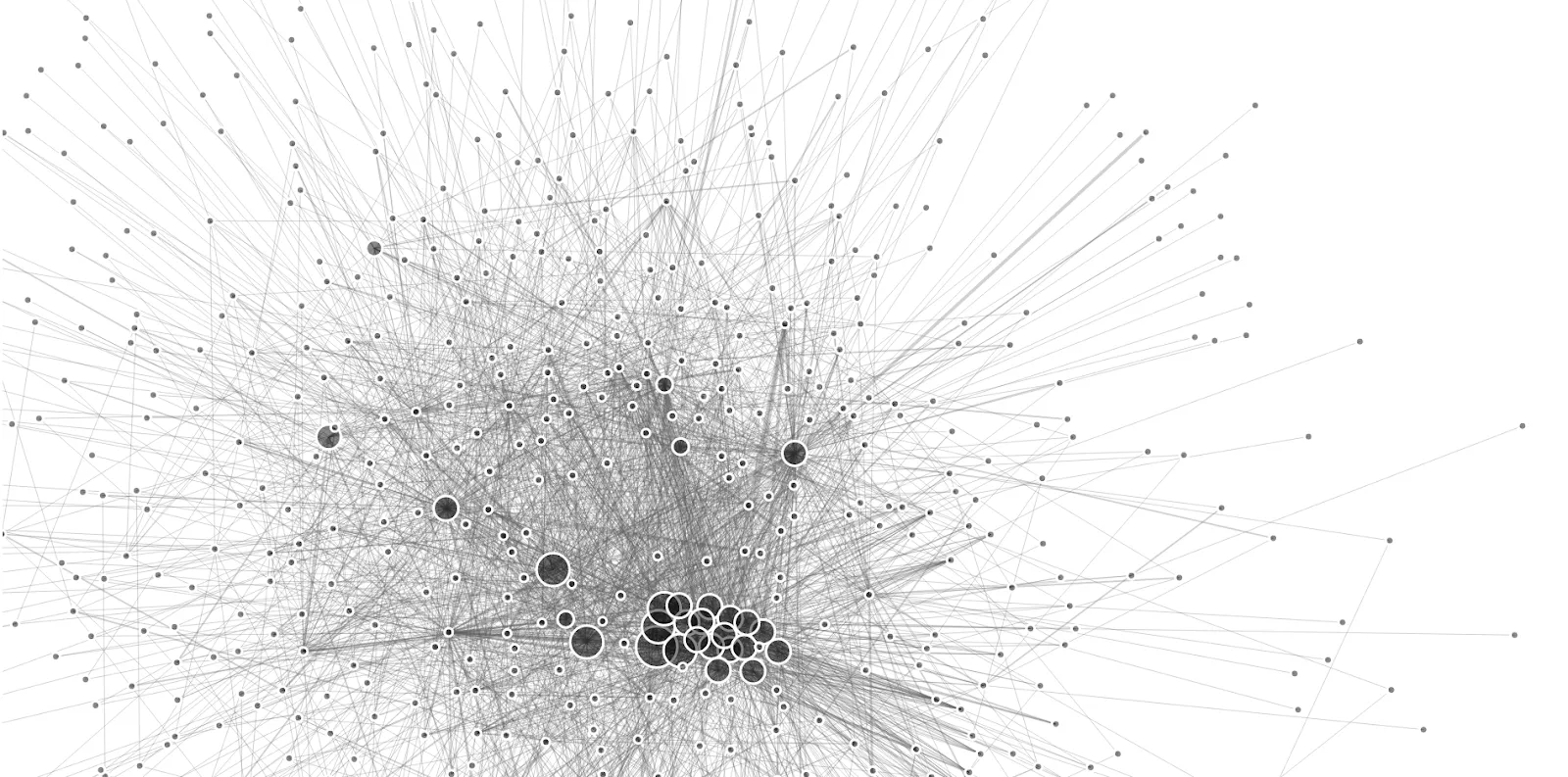

How big is the network?

It’s hard to grasp something that involves thousands of little parts, making millions of interactions with each other. It’s a bit like trying to picture everything going on in your brain. So, to make this a bit easier, we have used a number of visual diagrams. This is what the Lightning Network looks like from above.

A great resource for Lightning Network data is 1ML, a search and analysis engine. It provides data on which stores accept Lightning payments and information about current nodes. But it also features a spectacular visualization of the Lightning Network, showing all the nodes and how they are connected to one another. Check it out.

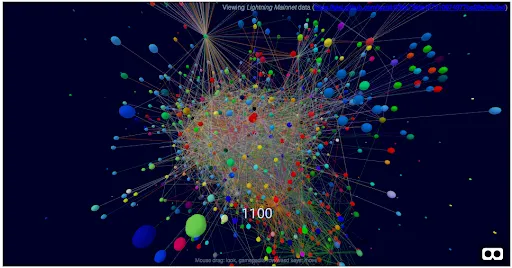

If that wasn’t trippy enough, here’s a 3D view of the Lightning Network you can explore. And if you want to dive even deeper inside the network, you can don VR glasses to get the full experience.

This visualization makes the Lightning Network look like some kind of futuristic planet. This is the view from one person’s node. The larger the areas, the more Bitcoin in the Lightning channels. Interestingly, the large blue area on the right is called “DeutscheTestnetBank,” whomever that might be.

The current state of the Lightning Network

The Network faced its first major hijack on March 20, 2018, when a distributed denial of service attack took down around 200 Lightning nodes, about 20% of the network at the time—the network struggled to process transactions. After preventative measures were put in place, it grew to reach a total of 7,000 nodes.

Since then, the Lightning Network has continued to grow. As of July 2023, there are about 16,000 Lightning nodes and over 70,000 channels in operation. The total network capacity of the Lightning Network now sits at 3,815 BTC (or around $113.2 million at current values).

Each Lightning node is responsible for interacting with the others to help transact money, while the channels are essentially the highways that enable money to be moved between nodes on the network. The more nodes and channels there are, the easier it is for larger transactions to complete successfully.

The future

The popularity of cryptocurrencies and transacting on them has, within just a few short years, put increasing stress on blockchains.

While there have been smaller changes—and in some cases forks—to help networks better cope with demand, the Lightning Network, if successful, could help open the door to widespread adoption of cryptocurrencies and their applications.

In August 2020, the Lightning Network was updated to include support for the Wumbo function. In the early days of Lightning, the developers limited how much Bitcoin could be kept inside a Lightning payment channel to 0.1677 BTC; Wumbo channels enable nodes to service larger transactions at higher volumes.

A growing number of crypto exchanges now support the Lightning Network, including Kraken, OKEx, Bitstamp and Bitfinex, as well as financial trading app Robinhood. However, two major exchanges, Binance and Coinbase, have yet to introduce support.

And in El Salvador, which in June 2021 passed legislation to make Bitcoin legal tender, vendors are using Lightning Network to facilitate small payments, while the state-sponsored Chivo wallet will also integrate Lightning Network. It's perhaps the first example of Bitcoin being used for widespread day-to-day transactions, and "the first deployment of Lightning at this scale," according to the co-founder of AlphaPoint, a developer working on the Chivo wallet.

In April 2022, Lightning Labs raised $70 million to fund development of the Taro protocol, which will help to enable stablecoin transactions on Lightning Network.

The Lightning Network is spreading beyond Bitcoin, too. Blockstream has created its own implementation of the Lightning Network called c-Lightning, which is built in the C programming language, familiar to most developers. Litecoin has its own version, too—the Litecoin Lightning Network—which is small compared to the Bitcoin version, but slowly growing.

For more on the Lightning Network, check out Jameson Lopp’s resources page here.